Xbox Cloud Gaming Equirements: Internet, Devices, Controllers

Xbox Cloud Gaming Equirements: Internet, Devices, Controllers  How to Delete Sent Messages on iPhone From Both Sides

How to Delete Sent Messages on iPhone From Both Sides  Portable Monitor For Laptop Guide

Portable Monitor For Laptop Guide  Optimizing Sales Prospecting with Modern Software Tools

Optimizing Sales Prospecting with Modern Software Tools  What Is One Way That Technology Can Improve The Distribution Of Goods?

What Is One Way That Technology Can Improve The Distribution Of Goods?  Xbox Cloud gaming: A Practical Guide For Real Life

Xbox Cloud gaming: A Practical Guide For Real Life  Game Pass vs PlayStation Plus: which is actually worth it?

Game Pass vs PlayStation Plus: which is actually worth it?  Macfox X1S installation guide: assembly, setup, and first ride checks

Macfox X1S installation guide: assembly, setup, and first ride checks

Introduction

Business insurance plays a crucial role in a company’s overall financial planning, serving as a proactive defense against a wide range of potential risks. By integrating the right coverage into your long-term strategy, your business can protect vital assets, maintain stability, and remain prepared for unforeseen challenges. Understanding why business insurance is essential for small businesses helps ensure continuity, minimize financial disruptions, and support sustainable growth. This strategic foundation empowers business owners to confidently pursue new opportunities, even amid economic uncertainty or industry shifts, ultimately positioning the company for long-term success in a competitive landscape.

A comprehensive approach to business insurance doesn’t just meet legal requirements—it provides critical peace of mind, knowing that your organization is equipped to handle lawsuits, property damage, employee injuries, and business interruptions. An intentional insurance strategy is a key component of responsible financial planning, helping to minimize uncertainty and foster sustainable growth. This fundamental layer of protection grants entrepreneurs and management teams the confidence to innovate and expand, secure in the knowledge that their investments and resources are shielded from potentially devastating setbacks.

Understanding Business Insurance

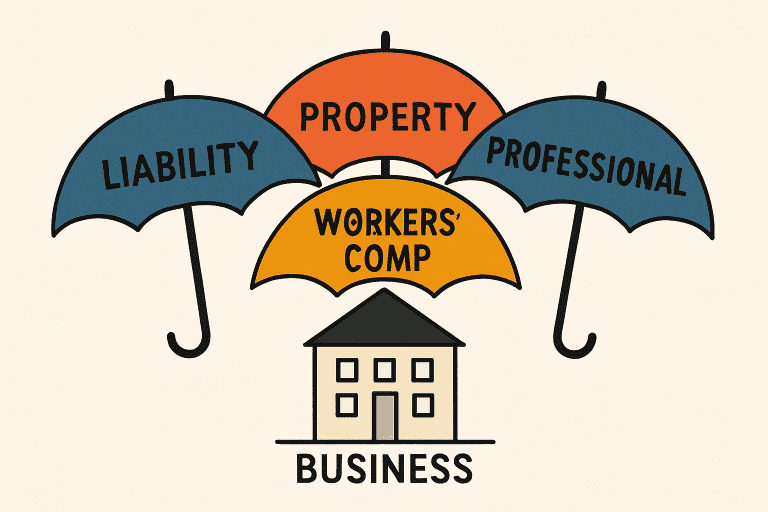

Business insurance is comprised of various policies tailored to shield companies from a host of risks and losses. The most common types of policies include:

- General Liability Insurance: Protects your business from legal claims, including bodily injuries, property damage, and advertising mistakes. It covers legal defense costs, settlements, and court-ordered fines if your company is liable. This insurance is foundational for any business because legal claims can originate from routine business operations or even accidental customer injuries on your premises.

- Property Insurance defends your company’s physical assets, such as buildings, equipment, and inventory, against losses from fire, theft, vandalism, or natural disasters. It is vital for maintaining productivity and quickly recovering from incidents that impact your workspace or valuable assets, ensuring business resilience and continued operations.

- Workers’ Compensation Insurance: Offers financial help and medical care for employees who are injured or become ill due to job-related incidents. It also protects businesses from potential lawsuits stemming from workplace injuries. In many regions, workers’ compensation is a legal necessity and signals your commitment to employee well-being.

- Professional Liability Insurance: Often called Errors and Omissions (E&O) insurance, it safeguards against claims of negligence, professional errors, or inadequate work that result in financial harm to a client. For service-based businesses, this policy is indispensable in maintaining credibility and protecting against high-stakes allegations that can affect your company’s bottom line and reputation.

Choosing an appropriate mix of policies is essential to ensure that every aspect of your business is protected from the most common—and costly—risks it may face. The right insurance foundation supports everything from internal operations to public reputation, making it crucial to understand the breadth of coverage available and to match your needs with each chosen policy.

Mitigating Financial Risks

No matter how carefully a business is managed, unexpected scenarios such as fires, natural disasters, lawsuits, or digital data breaches can result in significant financial strain. Comprehensive insurance coverage functions as a much-needed safety net in these situations, protecting not just tangible assets but also your employees, data, and long-term financial health.

For example, business interruption insurance helps businesses weather periods of halted operations by covering lost income and ongoing expenses until normal activity can resume. Such protection prevents a single unpredictable event from derailing your company’s finances and long-term plans. Without this type of insurance, businesses may struggle to pay rent, utilities, or staff salaries during periods where revenue halts, risking permanent closure.

Insurance also covers costs that would otherwise come directly from your company’s reserves, including repairs, lost inventory, legal expenses, and claims for damages or injuries. This preserves cash flow and allows for continued investment in growth opportunities. It ensures that instead of scrambling to assemble emergency funds or take on debt in the aftermath of a crisis, you can keep your core operations intact and focus on recovery or expansion strategies.

Ensuring Business Continuity

Sustainability and resilience are foundational to successful businesses, especially when crises occur. Insurance policies designed to maintain business operations—such as business interruption or extra expense coverage—ensure that a company can meet payroll, pay rent, and recover swiftly from damage or disruptions. This can be the difference between emerging stronger or folding under pressure for smaller companies or startups.

By reducing the risk of catastrophic loss or closure, these policies safeguard jobs, protect stakeholder interests, and help businesses recover their reputations and customer bases after disruptions. In this way, insurance facilitates strategic planning for continuity, providing a buffer during the most challenging times. It also demonstrates to creditors, investors, and partners that you are a deliberate and prudent leader, which can inspire confidence and continued support through adversity.

Enhancing Credibility and Compliance

Carrying the right insurance not only protects your operations but also speaks volumes to clients, suppliers, and partners. Having documented coverage sends a clear message that your business is responsible, trustworthy, and prepared for adversity. This is especially vital in sectors where competition is fierce and customers are increasingly selective about the businesses they partner with.

Many contracts and client relationships require proof of insurance, especially in industries where risk is heightened. Furthermore, certain types of coverage—such as workers’ compensation and liability insurance—are mandated by federal, state, or local laws. Maintaining compliance with these regulations avoids legal complications and costly fines, and keeps your business eligible to compete for valuable opportunities. Not only does this shield your company from potentially devastating financial penalties, but it also removes barriers to participating in larger projects and long-term contracts, which often demand proof of adequate insurance.

Tailoring Insurance to Your Business Needs

Every business has unique exposure to risk depending on its industry, location, size, and operational complexity. Conducting a careful risk analysis is the first step in customizing an insurance portfolio to fit your organization’s requirements. Assessing the risks tied to your workforce, facilities, digital infrastructure, and customer base ensures that your insurance spending directly supports the most vulnerable areas of your company.

Consulting with insurance advisors or specialists can help you identify gaps in coverage and create a policy mix that evolves alongside your business. This tailored approach ensures that your company’s resources are effectively protected no matter how your operations change or expand. As companies enter new markets, launch new products, or scale their workforce, an agile insurance framework is a powerful ally in controlling new or unforeseen risks.

Regular Review and Adaptation

Change is a constant in business, whether you’re adding new products, hiring more staff, or entering new markets. Regularly revisiting and updating your insurance policies is essential to maintaining suitable protection. This includes assessing whether your policies cover emerging technology risks, increased inventory, or new types of service offerings.

Annual policy reviews can help ensure your coverage reflects your business’s current size and risk profile. Adapting your insurance as your company grows strengthens financial planning and protects you from emerging threats or liabilities. A proactive review process, ideally in partnership with a knowledgeable insurance broker or advisor, means your protection never lags behind evolving business realities.

Conclusion

Business insurance is more than a shield against potential disasters—it’s a proactive tool that helps build a stable, adaptable, and credible organization. Integrating insurance into financial planning is essential for managing risks and achieving long-term objectives. By staying informed, tailoring your coverage, and regularly reviewing your policies, you can support sustainable growth and ensure your business is prepared for whatever the future may bring.